How to Get a Business Loan With Bad Credit

Bad credit? No problem. Learn how and where to get a business loan, plus funding alternatives with our helpful guide.

Realizing that your bad credit can get in the way of getting a business loan can really burst your business-building bubble. But don’t lose hope. A less-than-colorful credit score doesn’t mean that your business goals should be put aside. Thankfully, there are paths you can take to securing a loan for your business — even with bad credit.

Learn how to get a business loan with bad credit, where to get business loans with bad credit, and alternatives to business loans right here.

What Counts as Bad Credit?

When you apply for a business loan, many lenders will take your personal credit score into account. Personal credit scores are usually calculated using the FICO score, which ranges between 300 and 850. The higher your FICO score, the better.

Your business credit score is impacted by:

- Debts: Most credit reporting agencies consider how much of your available credit you use at any given time. Try to keep a lower ratio of credit you’ve been extended to the amount you owe to keep your credit utilization ratio strong.>/p>

- Payment history: Missed a few loan payments due to paying for business start-up costs, equipment, or other necessary items? This will impact your credit score. Keep paying bills on time to get that score up high.

- Old credit: The longer you’ve had a credit account open, the more credible you seem to lenders.

- New credit. Alternatively, if you’re opening a bunch of new credit lines at once, it’s a red flag that your business may be experiencing financial woes.

- Credit type: On the other hand, having multiple types of credit can increase your score — but only if you pay them off on time.

Anything below 670 is considered subprime, meaning lenders may doubt your ability to repay a business loan. Anything below 629 is considered bad credit, meaning that lenders may not approve you for a business loan at all. Some lenders accept people with credit scores of at least 530, but they may require higher fees and interest rates.

How To Get a Business Loan With Bad Credit

Now for the part you’ve been waiting for — the steps for getting a business loan, even if you have bad credit.

#1

Evaluate the Reasons You Need a Loan

Take some time to write out exactly why you need a loan for your business. You’ll need to include this on your loan application, but it’s also helpful for your own purposes. It will help you to parse out the reasons you require financing, to either start your business or keep it running smoothly. Here are some questions to should ask yourself:

- How will the loan make your business more successful?

- Are there alternatives to taking on a business loan?

- Is the loan necessary for your continued business operations?

You should only take on a loan if it will help your business thrive. If you can’t provide a clear roadmap about how the infusion of cash will help, it may be a sign that you shouldn’t take on a loan at this time.

#2

Run the Numbers

Lenders look at various elements when deciding whether to approve your loan application. One of these elements is your capacity to repay the loan, which takes into consideration things like household income, annual business revenue, cash flow, personal and business credit scores, and how long your business has been around.

The more revenue and time spent operating your biz — and the less debt you have — the more likely you’ll qualify for a loan, even with bad personal credit.

#3

Work That Paperwork

When you apply for a loan, you’ll need to prove that you are who you say you are, your business is what you say it is, and you and your business are capable of repaying debts. That means paperwork: personal and business tax returns, business financial records, accounting documents, and your business plan.

Creating a business plan is important whether you have a nonprofit, S corporation, or C corporation (or really any business structure). The business plan is your time to let your business dreams shine — as clearly and comprehensively as possible. Be sure to include a discussion of how the business generates revenue, how it will continue to, and why customers need your products or services.

Think of this as your Shark Tank moment: Why should lenders invest money in your idea? Your business plan should also include insights into your target customers, your marketing strategy to increase your customer base, and information about how your business is organized and run.

#4

Research Lenders

Once the paperwork is ready, it’s time to learn more about potential lenders. Bad credit doesn’t make it impossible to secure a business loan, but it does narrow the lending pool significantly. It’s important to compare different lending options to ensure you make the right choice for you and your business.

#5

Submit Your Loan Application

Armed with the necessary information and paperwork, go forth and fill out your chosen lender’s formal application. Most lenders have online application options for borrowers, meaning that applying for a loan — even with bad credit — is easier today than ever before.

Types of Business Loans for Bad Credit

Securing a small business loan with bad credit can be tough because you likely won’t be able to get traditional business loans from banks or loans guaranteed by the Small Business Administration (SBA). Still, there are several types of business loans that can work even if you have bad credit:

- Invoice factoring: Your business can sell any outstanding invoices to a factoring company for a percentage of the total amount. The company then takes over collections and gives your business some of the leftover invoice amount. This loan type is easier to acquire since it’s secured.

- Invoice financing: Similarly, you can borrow money by using outstanding invoices as collateral. Keep in mind that with this option, your business will be responsible for collections, and you’ll use this money to repay the loan.

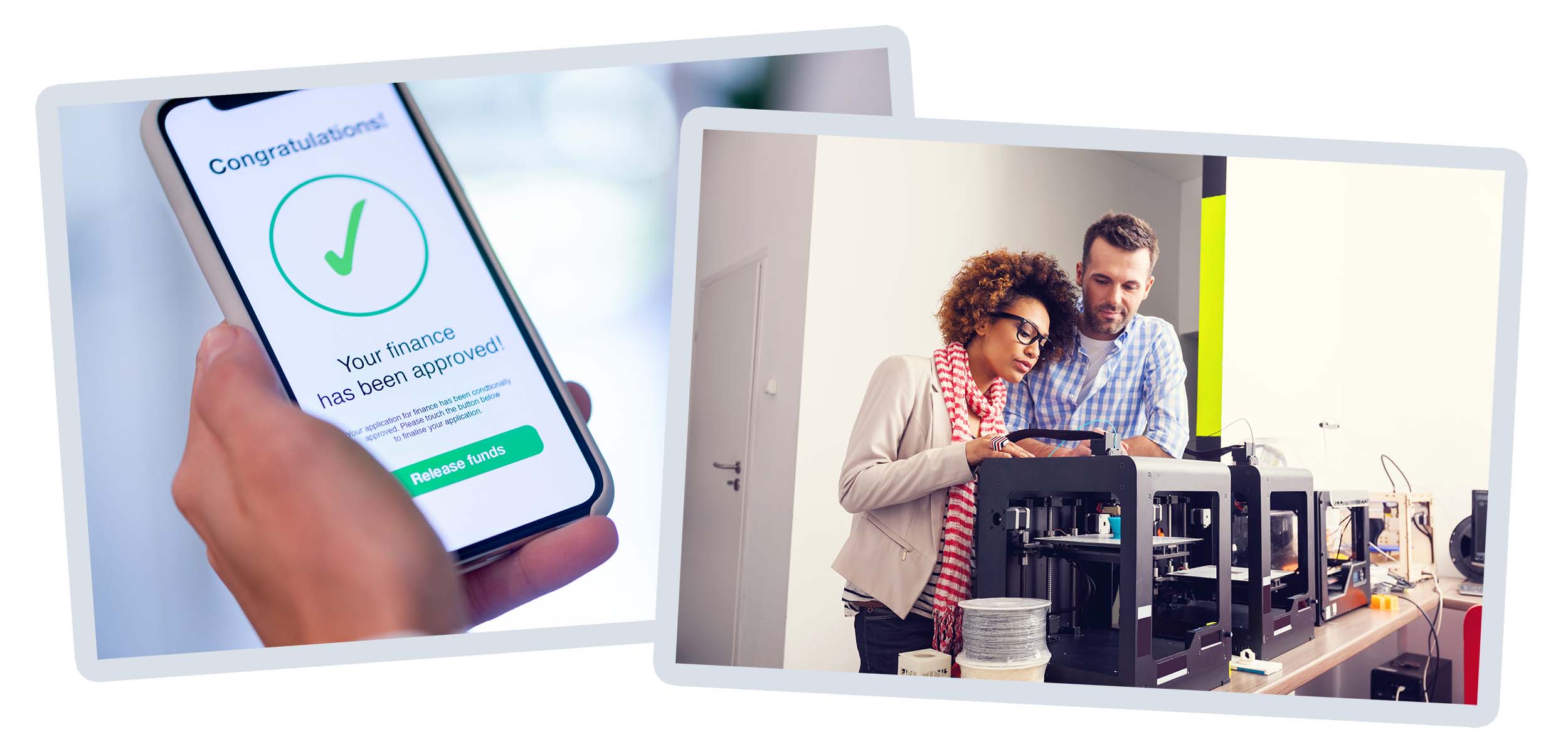

- Equipment financing: Do you only need money to buy 3D printers, specialty cupcake ovens, or other equipment for your business? Equipment financing allows you to borrow money specifically to use on equipment needed for your business — and the equipment itself is the collateral.

- Term loans: These loans allow your business to receive a lump sum of money, which you will eventually pay back to the lender. Annual percentage rates (APRs) for term loans are usually just under 10%.

- Business credit cards & lines of credit: Credit cards linked to your business allow you to use revolving credit limits to cover business-related expenses. APRs are high — around 25% — but only apply to ongoing balances.

- Merchant cash advances: If your business makes a lot of sales but you don’t have good credit, you can get a merchant cash advance by promising lenders part of future sales receipts.

Another thing to remember is that there is a big difference between loan qualifications across business structure types, like a sole proprietorship and an LLC or a corporation. If you have a sole proprietorship and need funding, you’ll need to register your business as an LLC or a corporation.

Where to Find Business Loans for Bad Credit

Where might you find a business loan lender, you ask? Here are some good options for getting a business loan with bad credit.

OnDeck: OnDeck offers short-term loans, like business lines of credit and term loans, for businesses with bad credit that struggle to qualify for a bank loan.

- Pros: The intuitive and quick application process means that you can acquire your loan as soon as the same day.

- Cons: OnDeck’s interest rates are quite high, with APR starting at 29%, and payment schedules can be aggressive.

- Minimum credit score: 625

Bluevine: Bluevine’s loaning process is start-up friendly, meaning that if you have a new business that needs money fast, it might be the right choice for you.

- Pros: Bluevine works with you to set loan term schedules for ongoing financial needs. They pay cash fast and allow borrowers who have at least half a year in business.

- Cons: Although their rates are lower than many other alternative lenders, they are still high compared to bank lenders, with APR starting around 15%. There’s also a borrower personal guarantee, which puts your personal assets on the line.

- Minimum credit score: 625

Fundera: Fundera provides an intuitive, user-friendly platform that matches small businesses with lenders.

- Pros: You only need to fill out one application to be sent out to a variety of potential lenders. Beyond simple efficiency, this also allows you to seek different types of loans. No collateral is required, and you can get funding within 24 hours of applying. Depending on the loan, the APR can start as low as 8%.

- Cons: Fundera isn’t a direct lender, which could cause communication issues. You’ll also have to pay Fundera fees.

- Minimum credit score: 575

Alternatives to Business Loans

If your credit score is too low for any of these loan options, or if you don’t like the idea of committing to a high APR, you may want to consider alternative funding options.

- Fintech: Lenders in the financial technology sector, like Fundbox, Kabbage, or LendingClub, may provide easy-access loans with better financing options.

- Angel investments: This kind of funding is great for those seeking start-up business loans with bad credit. The “angel” investors finance businesses in certain sectors (such as education or health care) that they believe are going places. In return, angel investors usually get a share of the business.

- Crowdfunding: Crowdfunding platforms, like Kickstarter, Fundable, or Indiegogo, allow businesses to raise capital from investors all over the world. Should you choose this financing route for your small business, be sure to have a clear business narrative and achievable funding goal. People donate to ideas they believe in, so make yours a compelling one and see how the crowd responds.

Building credit, both personally and in business, is not an easy process. Do the hard work and be prideful of the small and large accomplishments along the way. No matter what — work continuously to build your business credit so that your business looks attractive to future investors.

When you’re looking for financing, make sure to consult a small business financial planner. This professional can help you understand how to get a business loan with bad credit and what options will work best with your financial situation.

See other resources related to: